Last updated: June 2026

By CalcOrigin Editorial Team

What Is a Mortgage Calculator and Why You Need One

Think of a mortgage calculator as your home-buying reality check. Sure, it crunches numbers based on your home price, down payment, and interest rate. But a solid mortgage calculator does something more valuable. It stops you from falling in love with a house you can't really afford.

Here's what happens more often than you'd think. A first-time buyer sees a house listed at $400,000 and thinks, "I've got this." And maybe they do. But the monthly payment is what actually determines affordability. Not the sticker price. That payment includes principal, interest, property taxes, homeowner's insurance, and sometimes PMI and HOA fees on top of everything else. A good mortgage calculator catches all of that so you don't get blindsided later. That's the real value of a solid mortgage calculator.

The gap between knowing a home's price and understanding your full monthly obligation is surprisingly wide. That gap is where bad decisions happen. Run the numbers through a mortgage calculator before you start touring homes and you walk in with clarity. You know your limit, you stick to it, and you dodge the sting of realizing six months in that you're stretched too thin.

This matters even more in 2026. Rates aren't what they were a few years ago. A single percentage point difference in your rate can swing your payment by hundreds of dollars each month. Running a reliable mortgage calculator before you commit keeps it a smart financial decision rather than an emotional gamble.

How to Calculate Your Monthly Mortgage Payment

The math behind a mortgage payment isn't complicated, but it does look messy if you're staring at the formula for the first time. That's where a dedicated mortgage calculator saves the day. Here's the standard formula lenders use for fixed-rate loans:

M is your monthly payment. P is your loan amount. r is your monthly interest rate (just take your annual rate and divide by 12). n is the total number of payments over the life of the loan. A mortgage calculator does all this math in the background so you don't have to.

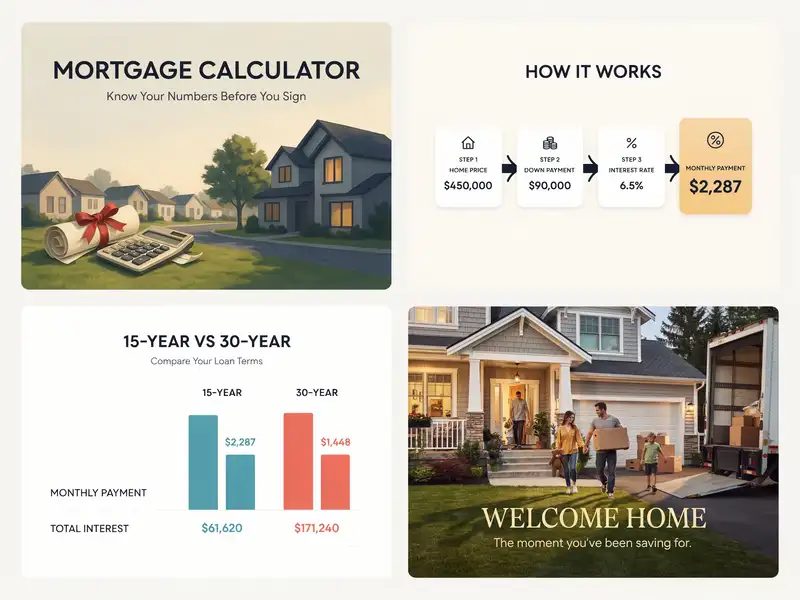

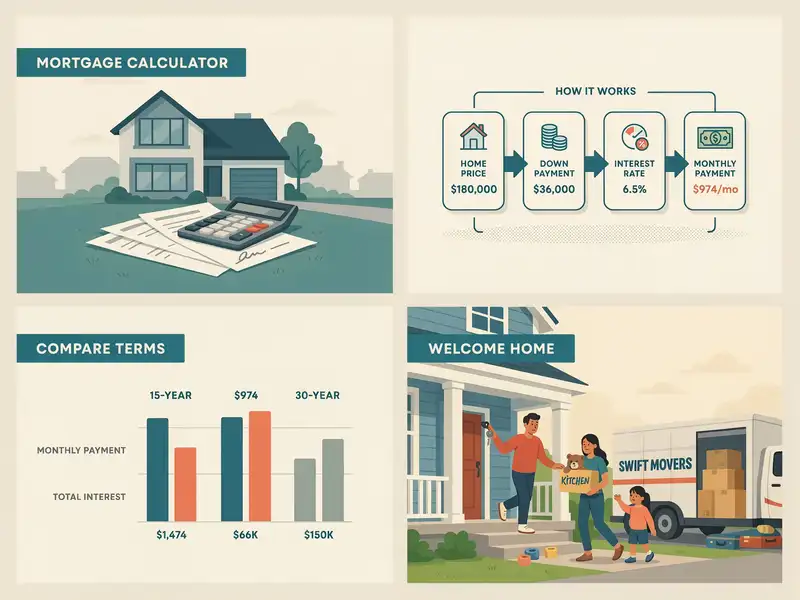

Let's try a real example. Say you're buying a $400,000 house with 20% down. Your loan comes to $320,000. On a 30-year fixed loan at 6.176%, your monthly interest rate works out to about 0.5147%, and you'll make 360 payments total. Plug all that in and your monthly principal and interest lands at roughly $1,950.

But here's the thing. That's not your full payment. You still have property taxes, homeowner's insurance, and other costs to add. If your annual property tax runs 1.2% of the home value and insurance costs $1,500 per year, that adds about $525 per month. Now you're looking at a true monthly cost of around $2,475. This is exactly why you want a mortgage calculator that accounts for everything.

Go ahead and try it with the mortgage calculator at the top of this page. Move the sliders around. Change the down payment, tweak the rate, add in the extras. The instant feedback makes it easy to compare different loan setups and see what works for your budget.

The Four Components of a Mortgage Payment

Lenders shorthand the four pieces of a mortgage payment as PITI: Principal, Interest, Taxes, and Insurance. Some loans add PMI and HOA on top, but PITI covers the core.

Principal

Principal is the money you actually borrowed. Every payment shaves a little off this balance. In the early years of a 30-year mortgage, only a sliver of your payment goes toward principal. As the balance drops, a bigger chunk of your payment starts eating into it. This gradual shift is called amortization, and it's why your loan balance doesn't move much at first.

Interest

Interest is what the lender charges you for the privilege of borrowing. They calculate it as a percentage of whatever you still owe. Early on, when the balance is highest, most of your payment is pure interest. That's not necessarily a bad thing if it means you got into a home years sooner than you could have otherwise. But it explains why your balance feels stubborn those first few years. A quality mortgage calculator shows how this split evolves over time.

On that $320,000 loan at 6.176%, the interest in month one comes to about $1,647. By year 15, the monthly interest drops below $1,000. By year 25, it's under $500. Watching those numbers shift is one thing that makes a good amortization calculator so useful.

Property Taxes

Property taxes are set by your local government based on your home's value. They pay for schools, roads, emergency services, and other community needs. Rates vary wildly depending on where you live. Texas homeowners pay relatively high property taxes. Hawaii homeowners pay among the lowest. Most lenders collect your property taxes as part of your monthly payment, hold them in an escrow account, and pay the bill when it's due.

Homeowner's Insurance

Homeowner's insurance covers your home and belongings against fire, storms, theft, and other disasters. Lenders won't let you skip it. Like property taxes, insurance premiums usually get paid through escrow each month. The average US homeowner pays between $1,200 and $2,000 per year, but your actual cost depends on where you live and how much coverage you want.

Additional Costs

Beyond PITI, there's more to factor in. PMI if your down payment is under 20%. HOA fees if your neighborhood has shared amenities. Maintenance costs that aren't part of the mortgage but hit your monthly budget anyway. A thorough mortgage calculator includes these line items so you see the real picture. Skip them and you might think you can afford more house than you actually can.

Understanding Mortgage Rates in 2026

Where do mortgage rates come from in 2026? A mix of Federal Reserve moves, inflation data, the bond market, and the overall economy. After the historically low rates of 2020 and 2021, things have settled into a different normal. Thirty-year fixed rates have found a range that feels high compared to a few years ago but is actually reasonable by historical standards.

Consider this. In the 1980s, mortgage rates peaked above 18%. Through the 1990s they hung between 7% and 10%. The 2% and 3% rates we saw in 2020 and 2021 were the anomaly, not the baseline. A 30-year fixed rate somewhere between 5.5% and 7% in 2026 looks pretty normal in the grand scheme of things. Punch those numbers into a mortgage calculator and you'll see they still work for many buyers.

Your personal rate depends on you. Lenders price loans based on risk, and lower-risk borrowers get better rates. The big factors are your credit score, how much you put down, the loan term you pick, the type of loan, and your property's location. Knowing these gives you some control over the rate you end up with.

Several key factors drive the rates lenders offer. The Federal Reserve's federal funds rate sets the baseline, influencing the cost of money across the economy. The bond market, specifically 10-year Treasury yields, closely tracks mortgage rate movements. Inflation data, employment reports, and broader economic conditions all feed into where rates land on any given day. When inflation runs hot, rates tend to rise. When the economy cools, rates typically fall. Understanding these forces helps you recognize when locking a rate makes strategic sense.

Your personal financial profile determines where you land within the current rate environment. Lenders evaluate your credit score, down payment amount, loan term, loan type, and property location to price your specific rate. A buyer with a 780 credit score and 25% down on a 15-year conventional loan will receive a much better rate than someone with a 660 score, 5% down, and a 30-year FHA loan. The difference between the best and worst rate for the same property on the same day can easily exceed one full percentage point.

Rate locks protect you while your loan processes. When you find a rate you are comfortable with, ask your lender to lock it for 30 to 60 days. This guarantees that rate even if market rates rise before closing. Some lenders offer float-down options that let you capture a lower rate if rates drop during your lock period, but this usually costs extra. Knowing when to lock versus float requires watching market trends and understanding your timeline.

A smart move is checking current rates before you start shopping. Our interest rate calculator shows you how different rates change your monthly payment, so you know what you're walking into before you talk to a lender. You can also use our mortgage calculator to see how those rates translate into a real monthly number. For a historical perspective, try our interest rate calculator to see how today's rates stack up against historical averages.

How Your Credit Score Affects Your Mortgage Rate

Your credit score ranks near the top of the list when lenders decide your rate. The gap between a 680 and a 760 can mean a rate difference of 0.75% to 1.25% or more. On a $320,000 loan, that's thousands of dollars in extra interest over time. A mortgage calculator makes this hit real by showing you exactly how your rate changes your monthly number.

Lenders group scores into tiers. Above 760 gets you the best rates. Between 700 and 759 still lands favorable terms. From 640 to 699 you can still qualify, but at higher rates. Below 640 gets tougher, though FHA loans exist for borrowers with lower scores.

If you're planning to buy in the next year, pull your credit report now. Give yourself time to fix mistakes and boost your score. Paying down credit cards, not opening new accounts, and paying everything on time are the simplest ways to move the needle. Run your numbers through a mortgage calculator to see what rate you should aim for.

Why Your Down Payment Matters Beyond the Initial Cost

A bigger down payment means a smaller loan, which lowers your monthly payment directly. But it also influences your interest rate and whether you need PMI. Most lenders like to see at least 20% down to drop PMI, though some conventional loans go as low as 3% down. Plug different down payment amounts into a mortgage calculator and the impact jumps right out.

Putting 20% or more down tells lenders you have real skin in the game. That lowers their risk, and they often reward you with a better rate. Even moving from 10% to 15% down can make a noticeable difference.

That said, waiting to save a full 20% isn't always the right call. Home prices in many markets climb faster than you can stash cash. A 5% or 10% down payment today might get you into a house that costs significantly more in a few years. Use our down payment calculator to figure out what makes sense for you, then pair it with a mortgage calculator for the full monthly picture. The mortgage calculator will show you how your down payment choice flows through to your payment.

15-Year vs 30-Year Mortgage: Which Is Right for You?

Every home buyer eventually faces this fork in the road. Both options have real trade-offs and neither is right for everyone.

A 30-year mortgage keeps your monthly payments lower by stretching them across more months. That makes it easier to qualify for a bigger loan and frees up cash for other things like retirement savings, an emergency fund, or home improvements. The catch is you pay dramatically more in total interest. On a $320,000 loan at 6.176%, the interest over 30 years comes to roughly $383,000. Our mortgage calculator can show you that in seconds.

A 15-year mortgage usually comes with a lower rate, sometimes 0.5% to 1% less than 30-year loans. You build equity faster and the total interest is way lower. On that same $320,000 loan at 5.382%, you'd pay about $147,000 in total interest. That's a savings of over $235,000. The trade-off? Your monthly payment is 40% to 60% higher.

So which way do you go? If you have steady income, a solid emergency fund, and you can handle the higher payment, a 15-year loan saves you a lot of money. If you'd rather invest the difference or you're stretching to afford the home, the 30-year gives you breathing room. Run both through the mortgage calculator and let the numbers guide you.

Fixed-Rate vs Adjustable-Rate Mortgages

A fixed-rate mortgage locks your interest rate for the entire loan term. Your principal and interest payment stays the same for 15 or 30 years, which makes budgeting dead simple. It is the most popular choice by a wide margin, especially when rates feel reasonable by historical standards. The main drawback is that you start with a higher rate than an ARM, and if market rates drop significantly, the only way to capture them is through refinancing, which costs time and money.

Adjustable-rate mortgages, or ARMs, start with a lower introductory rate that resets periodically based on a benchmark index plus a margin set by the lender. A common structure is 5/1, meaning the rate stays fixed for five years and adjusts once per year after that. Other options include 3/1, 7/1, and 10/1 ARMs. Most ARMs include adjustment caps that limit how much the rate can change at each adjustment and over the life of the loan. A typical cap structure is 2/2/5: the rate can adjust up to 2% at the first change, up to 2% per subsequent adjustment, and no more than 5% higher than the initial rate over the entire loan term.

ARMs can save you substantial money if you sell or refinance before the introductory period ends. The lower starting rate means lower payments during those first few years. The risk is that your payment increases when rates reset, potentially by hundreds of dollars per month. This is called payment shock, and it is the primary reason ARMs get a bad reputation. Borrowers who took out ARMs just before the 2008 housing crisis faced unaffordable resets when rates climbed and home values dropped simultaneously.

In 2026, the ARM vs fixed-rate decision depends on your timeline and risk tolerance. If you plan to stay in the home for less than 5 to 7 years, an ARM can save you thousands. If you plan to stay long-term or want maximum predictability, a fixed-rate loan is the safer choice. Some buyers use a hybrid approach: take a 30-year fixed for the lower payment and make extra principal payments to accelerate equity building. Run both options through this mortgage calculator to see how the numbers compare for your specific situation.

Amortization Schedule Explained

An amortization schedule is basically a play-by-play of your mortgage. It shows every single payment, how much goes to principal versus interest, and what's left on your balance after each one. Lenders use this same math to calculate your payoff timeline and interest totals.

In the early years, that schedule is heavy on interest and light on principal. Don't let that worry you. It's not a sign something is broken. It is just how amortization works. Interest gets calculated on a bigger balance, so it naturally consumes more of your payment. As the balance shrinks, the split flips and more of your money goes toward the principal. By the final years, nearly every dollar of your payment reduces the loan balance.

Here is a detailed breakdown of how the first 12 months look on a $320,000 loan at 6.176%. In month one, roughly $1,647 goes to interest and only $303 goes to principal. By month 12, the interest portion drops to about $1,633 and the principal rises to roughly $317. The shift is slow at first, but it accelerates over time as the balance compounds downward. This is the exact math your lender uses, and our amortization table on this page shows every single row of it.

The schedule has telling milestones worth understanding. On a 30-year $320,000 loan at 6.176%, you will not reach an even split between principal and interest until around year 22. By then you will have already paid over $290,000 in interest. By the final payment, almost all of it goes to principal. Seeing this play out in a mortgage calculator makes the long-term cost hit home in a way that a simple monthly payment number cannot.

You can view the full mortgage amortization schedule right here on CalcOrigin. Toggle between monthly and yearly views to zoom in or out. The yearly view is particularly useful for seeing big-picture progress, while the monthly view shows the gradual shift from interest-heavy to principal-heavy payments. Watching these numbers change is a powerful motivator to make extra payments when you can.

Private Mortgage Insurance (PMI) Explained

PMI stands for Private Mortgage Insurance, and here's the thing to understand right up front. It protects the lender, not you. If you default, the bank gets paid. You're the one footing the bill for it though.

PMI is required on conventional loans when your down payment is under 20% of the purchase price. It typically runs between 0.3% and 1.5% of your loan amount per year. On a $320,000 loan, that's roughly $80 to $400 per month. The exact cost depends on your credit score, your loan-to-value ratio, and the type of loan you get.

Here's the good news. PMI isn't forever. Once you reach 20% equity in your home, you can ask your lender to remove it. Under the Homeowners Protection Act, lenders have to automatically cancel PMI when your balance hits 78% of the original value, as long as you're current on payments. A reliable mortgage calculator factors PMI in so you see the full cost from day one.

If you're putting down less than 20%, make sure you include PMI when using a mortgage calculator. Some borrowers pay PMI upfront as a single premium at closing to keep monthly costs lower. Others go with a piggyback loan structure to avoid it entirely. Each option has pros and cons, so talk it through with your lender.

7 Tips for Getting the Best Mortgage Rate

Even a small improvement in your rate saves you real money. Here are seven ways to put yourself in the strongest position possible. Keep your mortgage calculator open and test each one as you go.

1. Improve Your Credit Score Before You Apply

Check your credit report for errors at least six months before you apply. Pay down your credit cards and don't open any new accounts. A score of 760 or higher puts you in the top tier for rates.

2. Save for a Larger Down Payment

Twenty percent or more eliminates PMI and signals lower risk. Even moving from 5% to 10% down can improve your rate a little. Every bit helps.

3. Shop Around with Multiple Lenders

Never take the first rate you're offered. Get quotes from at least three to five lenders. Big banks, credit unions, online mortgage companies. Studies show that borrowers who shop around save 0.25% to 0.50% on average.

4. Consider Paying Discount Points

Discount points let you buy a lower rate by paying an upfront fee. One point typically costs 1% of the loan amount and lowers your rate by about 0.25%. If you plan to stay in the home for several years, buying points can be a smart play.

5. Choose the Right Loan Term

Shorter terms like 15-year loans come with lower rates. If you can handle the higher payment, this alone saves you a lot over the life of the loan.

6. Lock Your Rate When the Time Is Right

Rates change daily. When you see one you're comfortable with, ask your lender about a rate lock. Most locks hold for 30 to 60 days and protect you from increases while your loan processes.

7. Keep Your Debt-to-Income Ratio Low

Lenders like to see a debt-to-income ratio below 43%, and lower is better. Pay down car loans, credit card balances, and student loans before you apply. It helps your rate and your chances of approval.

For a deeper look, try our payment calculator to run side-by-side comparisons of different rates and terms.

Mortgage Types: Conventional, FHA, VA, and USDA Loans Compared

Not all mortgages are the same. The type of loan you choose affects your rate, down payment requirement, credit score minimum, and overall cost. Understanding the differences helps you pick the right one for your situation. A mortgage calculator helps you compare payments across loan types once you know the typical rate for each.

Conventional Loans

Conventional loans are the most common type of mortgage. They are not backed by the government and typically require a credit score of 620 or higher. Down payments can be as low as 3% for first-time buyers, but you will pay PMI if you put down less than 20%. Interest rates on conventional loans are competitive, especially for borrowers with strong credit. These loans work well for buyers with good credit and a solid down payment saved up.

FHA Loans

FHA loans are insured by the Federal Housing Administration and designed for borrowers with lower credit scores or smaller down payments. You can qualify with a credit score as low as 580 and put down just 3.5%. If your score is between 500 and 579, you may still qualify with a 10% down payment. FHA loans require both an upfront mortgage insurance premium and annual MIP (mortgage insurance premium) for the life of the loan if your down payment is under 10%. These loans are popular with first-time buyers who have not yet built strong credit or large savings.

VA Loans

VA loans are available to active-duty military members, veterans, and eligible surviving spouses. They are backed by the Department of Veterans Affairs and offer some of the best terms available: zero down payment required, no PMI, competitive interest rates, and limited closing costs. You do need a Certificate of Eligibility and the lender will look for a credit score of 620 or higher. For eligible borrowers, VA loans are often the most affordable option by a wide margin.

USDA Loans

USDA loans are backed by the U.S. Department of Agriculture and designed for home buyers in eligible rural and suburban areas. They offer zero down payment financing for qualified borrowers. To qualify, your income must not exceed 115% of the area median income, and the property must be in a designated rural area. USDA loans require an upfront guarantee fee and annual fee, which functions similarly to mortgage insurance. Credit score requirements are typically 640 or higher.

Which loan type is right for you depends on your credit profile, your savings, and where you plan to buy. Use this mortgage calculator to estimate payments for different loan scenarios once you know which type fits your situation. You can also try our FHA loan calculator or VA mortgage calculator to explore specific loan type scenarios.

Making the Most of Your Mortgage Calculator

A mortgage calculator isn't something you use once and forget. It's a tool you come back to as your situation changes and you learn more about what you can afford.

Start before you even look at houses. Put your ideal budget into the calculator and see what comes out. If the monthly payment looks too high, adjust the numbers. Try a longer term, a bigger down payment, or a lower price range. The calculator helps you find the sweet spot before you're standing in a living room imagining your furniture there.

When you're getting closer to making an offer, use the mortgage calculator to compare scenarios. Should you put more money down and keep a smaller emergency fund? Try both. Should you take the 15-year loan or invest the difference? Run both numbers and compare.

After you close, revisit the calculator now and then. Got a bonus or tax refund? See what a one-time payment does to your loan. If rates drop, check whether refinancing makes sense. Our refinance calculator can help you figure out if a new loan would save you money after closing costs.

How to Qualify for a Mortgage in 2026: DTI, Credit, and Documentation

Qualifying for a mortgage in 2026 requires meeting several lender criteria. Understanding each one before you apply puts you in a stronger negotiating position and can save you money on your rate. Keep your mortgage calculator handy as you evaluate what you can afford.

Debt-to-Income Ratio (DTI)

Your DTI compares your monthly debt payments to your gross monthly income. Lenders calculate it by adding up your expected housing payment, car loans, student loans, credit card minimums, and other recurring debts, then dividing by your pretax income. Most lenders want to see a DTI below 43%, though conventional loans can go up to 50% with strong compensating factors. The lower your DTI, the better your rate and the more confidence the lender has in your ability to repay. Paying down credit cards and other debts before you apply is one of the fastest ways to improve this number.

Loan-to-Value Ratio (LTV)

LTV compares your loan amount to the appraised value of the home. If you put 20% down on a $400,000 home, your LTV is 80%. A lower LTV means less risk for the lender, which typically results in a better interest rate. LTV also determines whether you need PMI. Above 80% LTV means PMI is required on conventional loans. Understanding how your down payment affects LTV helps you plan how much to put down before you use this mortgage calculator.

Employment and Income Documentation

Lenders want to see stable, verifiable income. Expect to provide two years of W-2s, recent pay stubs, and bank statements. Self-employed borrowers need two years of tax returns and sometimes a profit-and-loss statement. Employment gaps or frequent job changes can raise red flags. The key is consistency. Lenders look for a two-year history of steady income in the same field. If you recently changed careers, waiting until you have a year of history in the new role can strengthen your application.

Assets and Reserves

Beyond your down payment, lenders want to see that you have cash reserves after closing. Two to six months of mortgage payments in reserve is typical, though requirements vary by loan type and lender. These reserves show you can handle unexpected expenses without missing a payment. Having strong reserves can also help you qualify for a better rate, especially if your credit score or DTI are on the borderline.

The Pre-Approval Process

A pre-approval letter from a lender tells sellers you are a serious buyer. Unlike pre-qualification, which is a casual estimate, pre-approval involves a credit check and document review. Getting pre-approved before you start house hunting gives you a clear budget and makes your offer more competitive. It also lets you lock in a rate estimate, which you can then plug into this mortgage calculator to confirm your monthly payment range before you start touring homes.

Common Mortgage Mistakes to Avoid

Even smart buyers trip up sometimes. Here are the mistakes worth making sure you don't repeat.

Focusing Only on the Interest Rate

The rate matters, but it's not everything. Origination fees, closing costs, discount points, and the APR all affect what you actually pay. A slightly higher rate with lower fees can sometimes be cheaper than a lower rate with heavy fees.

Not Accounting for All Monthly Costs

Some buyers only look at principal and interest. They forget about property taxes, insurance, PMI, and maintenance. Then the real payment hits and they wonder what happened. Always use a comprehensive mortgage calculator that covers every major expense. Ours does.

Making Big Financial Changes Before Closing

Lenders check your finances right up to closing. Taking on new debt, switching jobs, or making a big purchase can blow up your approval. Wait until after closing to finance a car, buy furniture on credit, or change careers.

Skipping the Home Inspection

Not required, but skipping it is a gamble. An inspection catches foundation cracks, old wiring, roof damage, plumbing problems. A few hundred dollars on an inspection can save you thousands in surprise repairs.

Not Comparing Multiple Lenders

We mentioned this earlier but it's worth repeating. People who shop around get better rates. Yet so many people take the first offer. Spend an afternoon getting multiple quotes from banks, credit unions, and online lenders. Studies show that borrowers who compare at least three lenders save 0.25% to 0.50% on their rate on average. Over 30 years, that can save you $10,000 or more. Use this mortgage calculator to compare the long-term costs of different offers side by side.

Ignoring Your Credit Score Until It Is Too Late

Your credit score plays a massive role in the rate you qualify for, yet many buyers do not check their score until they are ready to apply. Pull your credit report at least six months before you plan to apply for a mortgage. Dispute any errors, pay down revolving balances, and avoid opening new credit accounts. Even a 30-point increase can move you into a lower rate tier. Use this mortgage calculator to see how much a better rate saves you each month.

Overlooking First-Time Home Buyer Programs

Many states, cities, and lenders offer assistance programs specifically for first-time buyers. These can include down payment grants, reduced interest rates, tax credits, and lower mortgage insurance requirements. The eligibility criteria vary by location and income level. Research what is available in your area before you commit to a loan structure. Pairing a first-time buyer program with a conventional or FHA loan can significantly reduce your upfront and monthly costs. Run those numbers through this mortgage calculator to see the difference.

Final Thoughts

Buying a home is probably the biggest financial move you will ever make. The difference between a thoughtful mortgage and a rushed one can add up to hundreds of thousands of dollars over your lifetime. Taking the time to understand how the numbers work, what drives your rate, and how different loan structures play out is time you will not regret spending. Knowledge truly is money in this situation.

A mortgage calculator is the single best tool you have in this process. It lets you make decisions with your eyes open, compare scenarios honestly, and plan your finances with confidence. Whether you are buying your first home, moving up to a larger property, or refinancing your existing mortgage, running the numbers before you sign is always the right call. Small changes in your down payment, loan term, or interest rate can produce surprisingly large differences in your total cost.

Start with the calculator at the top of this page. Adjust the inputs, try different combinations, and see how small changes ripple through your monthly payment and long-term interest costs. Compare a 15-year against a 30-year. See what happens when you add an extra $100 per month. Check how much a lower rate saves you. The more you explore with this mortgage calculator, the better you will understand how mortgages actually work. And the better you understand them, the more likely you are to make a choice that works for your budget and your future.

Bookmark this page and come back to it throughout your home-buying journey. Run updated numbers as rates change, as your savings grow, and as you narrow down your price range. A well-informed buyer makes better decisions, and this mortgage calculator is here to help you every step of the way.